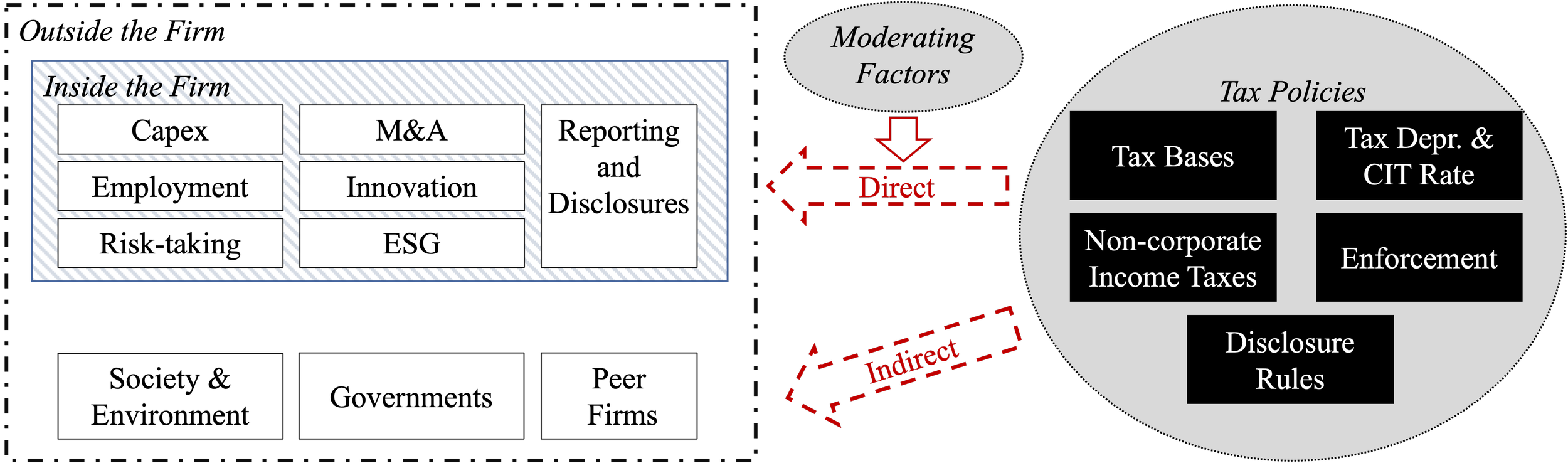

Professor Lester’s research studies the role of tax policies in firms’ investment and employment decisions.

Tax policy changes are often intended to stimulate economic growth by motivating companies to increase investment spending and hire more workers. Prior research generally finds that tax policies can indeed lead to these real investment and employment effects, but researchers face serious challenges when disentangling these effects from financial reporting effects and other economic responses that can accompany them.

Professor Lester’s research documents and quantifies the role of reporting incentives, disclosure regimes, and information frictions in the effectiveness of tax incentives. Her work shows that information incentives and frictions play a critical role in either facilitating the implementation of or — in some cases, delaying the corporate response to — cross-border, national, and local tax regimes.

Published and ongoing research focuses on three elements of tax policies:

National and International Tax Regimes and Incentives (jump to research)

State & Local / Place-based Tax Incentives (jump to research)

Tax Status: Tax Losses and Non-Corporate Entities (jump to research)

Other related work (jump to research)

National and International Tax Regimes and Incentives

The Effect of Repatriation Tax Costs on Multinational Investment

With Michelle Hanlon and Rodrigo Verdi, 2015.

Journal of Financial Economics, Vol. 116, Issue 1, 179-196.

This paper investigates whether the U.S. repatriation tax for U.S. multinational corporations affects foreign investment. Our results show that the locked-out cash due to repatriation tax costs is associated with a higher likelihood of foreign (but not domestic) acquisitions. We also find a negative association between tax-induced foreign cash holdings and the market reaction to foreign deals. This result suggests that the investment activity of firms with high repatriation tax costs is viewed by the market as less value-enhancing than that of firms with low tax costs, consistent with foreign investment of firms with high repatriation tax costs possibly reflecting agency-driven behavior.

Made in the USA? A Study of Firm Responses to Domestic Production Incentives Sole-authored, 2019.

Recipient of the MIT Sloan Best Dissertation Award and ATA/PwC 2016 Outstanding Tax Dissertation Award.

Journal of Accounting Research, Vol. 57, Issue 4, 1059-1114.

How do U.S. companies respond to incentives intended to encourage domestic manufacturing? I study the Domestic Production Activities Deduction (DPAD), which was enacted in the American Jobs Creation Act of 2004 and was the third largest U.S. corporate tax expenditure as of 2017. Using confidential data from the U.S. Bureau of Economic Analysis, I find greater average domestic investment spending of $95.5-143.6 million, but only within the sample of domestic-only firms and not until 2010, when the greatest statutory DPAD benefits were available. Additional evidence suggests that U.S. multinational claimants invest abroad rather than in the U.S. and that the increased investment by DPAD firms is accompanied by a reduction in the domestic workforce, consistent with a substitution of capital for labor. I show that the delayed investment response is due to firms engaging in other responses first, such as changing corporate reporting to shift income across time and borders. Quantifying the extent of these effects contributes to the literature that studies this tax deduction and informs policy makers as to the effectiveness of both manufacturing incentives and U.S. corporate income tax rate reductions in stimulating real domestic activity.

Which Companies Use the Domestic Production Activities Deduction?

With Ralph Rector, 2016.

Tax Notes, Vol. 152, Issue 9, 1269-1292.

This paper uses IRS C corporation 2012 tax return data to study the firms that claim the Sec. 199 deduction, thereby providing empirical evidence on the economic significance of the deduction and the characteristics of the companies that benefit from this incentive. The descriptive analyses show that, while the number of firms claiming Sec. 199 benefits is small, these firms are an economically important subset of all corporate firms and report over half of total positive corporate taxable income. Furthermore, corporations report that approximately $440 billion of taxable income qualifies for the deduction, equal to one-third of all corporate taxable income. Additional analyses show that approximately 72% of the deduction is claimed by large, multinational public firms with assets greater than $1 billion. While described as a tax deduction for domestic producers and manufacturers, only 60% of the deduction is claimed by firms in industries traditionally considered to generate production-related income. The statute has thus been applied widely by a number of firms in other industries who have identified some portion of their business that generates qualifying income. We also present data on how the statutory limitations within Sec. 199 reduce the number and extent to which firms claim the deduction, and we show how the number of firms and the amount of benefit claimed has changed over time.

Transparency and Tax Evasion: Evidence from the Foreign Account Tax Compliance Act (FATCA)

With Lisa De Simone and Kevin Markle, 2020.

Journal of Accounting Research, Vol. 58, Issue 1, 105-153.

We examine how U.S. individuals respond to regulation intended to reduce offshore tax evasion. The Foreign Account Tax Compliance Act (FATCA) requires foreign financial institutions to report information to the U.S. government regarding U.S. account holders. We first document an average $7.8 billion to $15.3 billion decrease in equity foreign portfolio investment to the United States from tax‐haven countries after FATCA implementation, consistent with a decrease in “round‐tripping” investments attributable to U.S. investors’ offshore tax evasion. When testing total worldwide investment out of financial accounts in tax havens post‐FATCA, we find an average decline of $56.6 billion to $78.0 billion. We next provide evidence of other important consequences of this regulation, including increased expatriations of U.S. citizens and greater investment in alternative assets not subject to FATCA reporting, such as residential real estate and artwork. Our study contributes to both the academic literature and policy analysis on regulation, tax evasion, and crime.

U.S. Inbound Equity Foreign Portfolio Investment

The Effect of Innovation Box Regimes on Investment and Employment Activity

With Shannon Chen, Lisa De Simone, and Michelle Hanlon, 2022.

The Accounting Review, Vol. 98, Issue 5, 187-214

We study whether innovation box tax incentives, which reduce tax rates on innovation-related income, are associated with increased fixed asset investment and employment. Using a stacked cohort difference-in-differences design on an entropy-balanced sample of European multinationals, we find innovation box regimes are associated with higher levels of capital expenditures, relative to non-innovation box jurisdictions. We do not find discernable effects on total employment or total compensation. However, the data suggest that companies in innovation box countries have a more highly-compensated workforce following innovation box implementation, particularly among patent-owning observations in countries with more restrictive innovation box regimes and greater tax benefits. Our study contributes to the literature on, and policy evaluation of, innovation box regimes by examining the extent to which these incentives result in tangible investment and employment and by identifying how different characteristics of innovation box regimes impact these outcomes.

Tax Accounting Research on Corporate Investment: A Discussion of The Impact of IP Box Regimes on the M&A Market by Bradley, Ruf, and Robinson.

Journal of Accounting & Economics, Vol. 72, Issues 2-3.

In The Impact of IP Box Regimes on the M&A Market, Bradley, Robinson, and Ruf (2021) study whether and to what extent tax incentives for intellectual property affect corporate M&A investment activity. The paper finds that a 1.0 percentage point tax benefit leads to a 1.2% increase in M&A activity in a country after the implementation of an Intellectual Property (IP) Box tax regime. Results vary based on country-specific IP Box requirements, as well as firm-specific characteristics such as patent ownership and acquirer nationality. My discussion offers more cautious interpretations of the empirical results related to statutory country-specific requirements of these regimes and raises concerns about the type and timing of firm responses. More generally, I outline how this paper and other work by tax researchers in Accounting contributes to the broader literature studying the relation between corporate tax policies and investment activity.

Corporate Tax Policy in Developed Countries and Economic Activity in Africa With Jeff Hoopes, Daniel Klein, and Marcel Olbert, 2023.

Stanford Institute for Economic Policy Research Working Paper 23-27

This paper studies whether tax policies in developed nations affect developing economies. We study firm investment responses to a major reform that reduced the corporate income tax rate for U.K.-based firms. Our identification strategy compares subsidiary investment by U.K. multinational firms in Africa to those of multinationals with non-U.K. parent entities but similar ties to Africa. Difference-in-differences estimates show that U.K. multinational firms increased their subsidiary presence in sub-Saharan Africa by 22-28% following the U.K. reform. Exploiting location-specific nighttime luminosity data as well as local data from the African Demographic and Health Surveys, we also document increased economic activity and higher employment rates of African citizens within close proximity of local U.K.-owned subsidiaries. These effects are confirmed using novel data on local asset wealth. Our findings imply that, beyond the goal of motivating home-country investment, developed countries' corporate tax policies impact developing nations.

IPOs and Foreign Tax Structures

With Christine Dobridge and Andrew Whitten, 2025

Conditionally Accepted, The Accounting Review

Does going public affect the amount and type of corporate international tax planning? Using a panel of U.S. corporate tax return data from 2004 to 2018, we show that IPO completion is associated with the rapid implementation of multinational foreign tax structures. Specifically, within three years after filing for an IPO, firms (i) expand their presence in low-tax jurisdictions, (ii) enter into cross-border agreements that accompany intangible asset transfers to foreign subsidiaries, and (iii) increase their level of foreign related-party payments. Effects are strongest among firms with strong capital market pressure to hit post-IPO earnings targets, firms with high R&D spending pre-IPO, and firms with limited ability to use net operating loss carryforwards. We contribute to the nascent literature studying tax implications of IPOs by documenting the types and timing of specific tax strategies that enable public firms to remain lightly taxed in the post-IPO period.

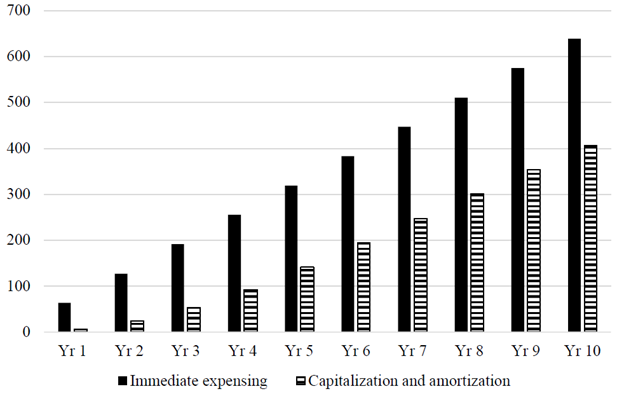

The Consequences of Changing the Tax Treatment of R&D

With Mary Cowx and Michelle Nessa, 2025

Revising for third round review, Journal of Accounting & Economics

We study the effects of limiting the tax deductibility of research and development (“R&D”) expenditures. From 2022 through 2024, U.S. companies were required to capitalize and amortize R&D rather than immediately deduct these expenditures. We use variation in U.S. firms’ fiscal year ends to examine the extent of—and heterogeneity in—firms’ responses to the R&D tax change in a difference-in-differences framework. We first document that affected U.S. firms’ cash effective tax rates increase by 9.6 to 10.9 percentage points (47.5% to 56.8%). Second, we find that R&D investment declines in response to the change; we estimate an aggregate reduction of $42 billion in the first year of the policy. This reduction is concentrated among research-intensive, domestic-only, and financially constrained firms. Third, we estimate decreases in domestic R&D employment of 1.4% to 2.6%, relative to domestic non-R&D employment. Finally, we observe decreased capital expenditures and share repurchases among affected companies, consistent with the R&D tax change impacting firms’ other investing and financing decisions. This paper provides policy-relevant evidence regarding the significant real effects of limiting the R&D tax deduction, which is an important but understudied innovation tax incentive.

State & Local / Place-based Tax Incentives

What Determines Where Opportunity Knocks? Political Affiliation in the Selection of Opportunity Zones.

With Mary Margaret Frank and Jeff Hoopes, 2022.

Journal of Public Economics 206 (2022) 104588

We examine the role of political affiliation during the selection of Opportunity Zones, a place-based tax incentive enacted by the Tax Cuts and Jobs Act of 2017. We find governors are on average 7.6% more likely to select a census tract as an Opportunity Zone when the tract’s state representative is a member of the governor’s political party. This effect is incremental to local demographic factors that increased the likelihood of selection, such as lower income levels and preceding improvements in local conditions. Selection of politically affiliated tracts is greatest in Republican-governed states, where the effect increases to 13.2%. Furthermore, we find procedures used by some governors when selecting Opportunity Zones - proportional allocation across a state and delegation of initial nominations to local authorities - offset the role of political affiliation. These results enhance our understanding of the selection of place-based economic incentives, providing evidence relevant for concurrent and future academic research and legislative proposals.

Opportunity Zones: An Analysis of the Policy’s Implications

With Cody Evans and Hanna Tian, 2018.

State Tax Notes, Vol. 90, Issue 3, 221-235.

This article summarizes the Opportunity Zone incentive in the Tax Cuts and Jobs Act by providing descriptive statistics on the selected zones, outlining considerations for investors, and using data on the New Markets Tax Credit to inform expectations of investors' responses to this policy.

Tax Subsidy Disclosure and Local Economic Effects

With Lisa De Simone and Aneesh Raghunandan, 2024.

Journal of Accounting Research, Vol. 63, Issue 2, 547-598.

We examine if the effectiveness of business tax subsidies varies based on state disclosure laws. The prior accounting literature on government disclosure documents substantial variation in the quality of such disclosures, raising questions about their effectiveness for monitoring. State and local business subsidies for investment and employment have tripled in size over the past 30 years, but transparency problems inhibit clear assessments of whether subsidies achieve their intended outcomes. We examine both internal disclosure laws, which mandate subsidy reporting by the granting state agency to other state oversight agencies, and external disclosure laws, which mandate reporting to the public. We find positive effects of subsidies on local employment when subsidies are subject to internal disclosure laws; by implementing such regimes, governments could forego 1.2–1.7 subsequent subsidies per county, saving $419.0–$593.5 million in aggregate. In contrast, we observe little effect of external disclosure, which we show is due to governments either substituting to other types of incentives or posting stale information that impedes public monitoring. We contribute to the government disclosure literature by demonstrating the real employment effects of internal government disclosures, and we provide policy-relevant evidence about the conditions under which external disclosure regimes facilitate public monitoring.

Tax Status: Corporate Tax Losses and Non-Corporate Entities

Taxation and Corporate Risk-Taking

With Dominika Langenmayr, 2018.

Recipient of the 2021 ATA Outstanding Manuscript Award.

The Accounting Review, Vol. 93, Issue 3, 237-266.

We study whether the corporate tax system provides incentives for risky firm investment. We analytically and empirically show two main findings: first, risk-taking is positively related to the length of tax loss periods because the loss rules shift some risk to the government; and second, the tax rate has a positive effect on risk-taking for firms that expect to use losses, and a weak negative effect for those that cannot. Thus, the sign of the tax effect on risky investment hinges on firm-specific expectations of future loss recovery.

Tax Loss Measurement.

With Shane Heitzman, 2021.

National Tax Journal, Vol. 74, Issue 4, 867-893.

We use financial disclosures to develop a novel proxy for net operating loss carryforward (NOL) tax benefits. This approach more accurately identifies firms with tax losses, more precisely measures the tax loss, and better predicts reductions in future taxes than existing proxies. We derive a prediction model, which future researchers can employ to better approximate the NOL tax benefits based on readily available financial data. We also demonstrate how NOL nonlinearity affects measurement of corporate tax status. By proposing a new measure and demonstrating trade-offs across competing proxies, we contribute to the work in public economics, corporate finance, and tax accounting that examines the responsiveness of the business sector to corporate tax incentives.

Net Operating Loss Carryforwards and Corporate Savings Policies

With Shane Heitzman, 2022.

The Accounting Review 97(2), 267-289.

We examine the relation between corporate cash holdings and tax net operating loss carryforwards (NOLs). The literature demonstrates that firms should distribute cash to shareholders rather than retain it and generate passive investment income taxed at both corporate and investor levels. However, if the firm’s tax rate on passive income is lower than shareholders’—as when the firm has NOLs—theory also shows that the firm should retain cash and invest on the shareholders’ behalf. Consistent with this, we find that NOLs are associated with higher levels of savings; firms save an additional $0.12 to $0.17 per dollar of tax-effected NOL benefit. Furthermore, investors place a higher value on corporate cash in tax loss firms, consistent with NOLs increasing the after-tax returns on passive investments. The paper adds to the literature studying corporate financial policy responses to taxation and quantifies the role of NOLs in corporate savings decisions.

The Spiderweb of Partnership Tax Structures

With Ryan Hess, Emily Black, Zaynah Javed, Jonathan Hennessy, Jacob Goldin, Dan Ho, and Annette Portz, 2024.

Working paper.

U.S. partnerships control more than $40 trillion in assets, vastly outnumber U.S. public firms, and contribute significantly to the U.S. tax non-compliance of pass-through entities, which is larger than the non-compliance of publicly traded corporations. However, the prior literature provides extremely little evidence explaining the pervasive use of such entities and which specific characteristics enable the lightly taxed nature of partnership business income. Using administrative U.S. tax data, we first create graphical organizational structures by tracing income through millions of partnership entities. We show that 80 percent of partnership groups are simple structures composed of one single partnership owned directly by individual taxpayers. In contrast, the most complex structures resemble "webs," characterized by multiple tiers of ownership and clusters of overlapping partners. Second, we determine the entity attributes associated with partnerships developing into complex organizations. Third, conditional on being selected for audit, complex partnerships are four percent less likely to be assessed additional tax, but the amount of assessments is larger. Fourth, we show that complex partnership audits have a high return-on-investment, generating $20 of assessments for each $1 spent, which is a rate over eight times that for corporations. Thus, beyond adding to the nascent literature explaining the prevalent use of partnerships, we provide new insights about the under-reporting of tax on U.S. business income and quantify the potentially large increases in tax revenue collection that could be obtained from increased enforcement of complex partnership businesses.

Other Work

Firm’ Real and Reporting Responses to Business Taxation: A Review

With Marcel Olbert, 2025.

Journal of Accounting and Economics, Vol. 80, Issues 2-3.

Taxation is a central economic policy tool, with governments increasingly using tax policy to stimulate local economic growth and also regulate multinational firms. We review the empirical literature that studies the effect of tax policies on firms’ investment, employment, and other real outcomes. Building on the neoclassical theory of corporate taxes and tangible investment, we propose an organizing framework for our review that captures the wide set of tax policies and firm responses examined in accounting research. This framework highlights four dimensions along which accounting scholars contribute to the literature: (i) documenting the role of financial reporting incentives as a moderating factor in firms’ real responses, (ii) studying firms’ reporting versus real responses, (iii) quantifying real effects of tax disclosure regulations, and (iv) improving measurement of firms’ tax status and proxies for investment and employment. We identify open questions for future research and suggest new international, federal, and local settings that may help uncover underlying mechanisms driving observed economic phenomena. Specifically, we encourage scholars to further distinguish firms’ reported and real responses to tax changes and improve measurement of these outcomes, especially in settings related to environmental taxation or settings in which tax avoidance and real outcomes are closely linked.

U.S. Equity Crowdfunding: Real Effects of Financing Small Entrepreneurs

With Douglas Laporte, 2024.

Working paper

Equity crowdfunding allows small businesses to raise capital from the public via online platforms. We find that, despite having limited impact on diversifying entrepreneurship, it improves access to capital by financing younger firms compared to banks. Using the number of competing offerings as an instrument for equity crowdfunding success, we show that equity crowdfunding alleviates financial constraints of viable businesses. Successful issuers survive longer, are more likely to receive venture capital, and exhibit subsequent financial growth. We also find that equity crowdfunding activity is associated with both increased interest in entrepreneurship and increased venture capital investment in the local area.

Financial Flexibility and Corporate Employment Actions.

With Ethan Rouen and Brady Williams, 2021.

Working paper

We study the role of financial flexibility on firms’ workforce reduction decisions during a time of extreme economic uncertainty. Using daily data from the start of the COVID-19 pandemic —March through May 2020 — for 354 of the largest U.S. employers, we first descriptively show that negatively shocked firms were 39.2 percentage points more likely to reduce their workforce than positively shocked firms. Our central finding is that pre-pandemic financial flexibility significantly reduces the likelihood of workforce reductions. We further demonstrate that the attenuating role of financial flexibility is greatest among firms with better governance and those with more asymmetric cost structures. Firms with stronger pre-pandemic commitments to employees are more likely to retain workers, regardless of their financial flexibility. These results provide insights on both financial and non-financial characteristics influencing workforce decisions, thereby informing managers about employment decisions in times of economic uncertainty.

The Role of Accounting in the Financial Crisis

With SP Kothari, 2012.

Accounting Horizons, Vol. 26, Issue 2, 335-352.

The advent of the Great Recession in 2008 was the culmination of a perfect storm of lax regulation, a growing housing bubble, rising popularity of derivatives instruments, and questionable banking practices. In addition to these causes, management incentives, as well as certain US accounting standards, contributed to the financial crisis. We outline the significant effects of these incentive structures, and the role of fair value accounting standards during the crisis, and discuss implications and relevance of these rules to practitioners, standard-setters, and academics.